‘Wall Street and Washington, D.C., Are More Tightly Intermeshed With Each Other Than Ever,’ Expert Says

The absorption of First Republic Bank by JPMorgan Chase on May 1 was just the latest step in a relentless march of consolidation among U.S. banks, as America’s banking industry becomes both more concentrated and more closely entwined with the federal government.

Since the “Great Financial Crisis” of 2008, federal regulators have become comfortable with a banking industry led by a handful of mega-banks, with which agencies have an ever-closer working relationship.

The strategy of bank regulation has been to allow the banking industry to consolidate into an ever-smaller number of ever-larger institutions, which are then subject to tighter regulation, higher capital requirements and various stress tests. This theoretically makes the banking system more robust and less prone to financial crises.

The close relationship between federal agencies and banks has featured, for example, collaboration between regulators and banks like JPMorgan Chase, Citibank, Bank of America and Wells Fargo on a $30 billion fund in a failed attempt to prop up First Republic bank. It also included surveillance conducted by Bank of America for the FBI in a warrantless search of customer accounts to track travel and purchase records during the Jan. 6, 2021, riots at the U.S. Capitol.

Many who study America’s banking industry say that consolidation will inevitably continue and that the recent failure of several regional banks is merely the latest chapter in this saga. Others worry that having the country’s financial system so heavily concentrated in a handful of “universal” banks that are now “too big to fail” brings its own set of systemic risks, and that banks have now become too closely aligned with the federal government.

“You only need to recognize that much of Dodd-Frank was effectively written with the assistance of people working at prominent banks to know that this is the case,” Samuel Gregg, a political economist at the American Institute for Economic Research, told The Epoch Times.

The Dodd-Frank Act, passed in 2010 in response to the global financial crisis of 2008, promised to protect the American taxpayer by ending bailouts and reducing exposure from too-big-to-fail banks. While the Dodd-Frank Act has increased regulatory control, it has failed to reduce the financial system’s exposure to single institutions. Rather, it has done the opposite.

“[Dodd-Frank] benefited large banks at the expense of small and medium-sized banks,” Gregg said. “Wall Street and Washington, D.C., are more tightly intermeshed with each other than ever.”

Speaking at a financial regulation conference on April 14, Federal Reserve Governor Michelle Bowman stated that the number of banks in America has been cut in half in the past two decades and that the formation of new banks “has essentially stagnated … limiting the availability of banking services to underserved communities.”

Despite the recent failures of three regional banks, Bowman said that “the smallest banks often outperform larger banks during periods of stress, like the pandemic and during the 2008 financial crisis.

“Historically, during times of economic and financial stress, the smallest institutions have performed extremely well,” she said. “For example, small banks demonstrated this strength during the pandemic through their outsized commitment to supporting small businesses.”

According to Michael Hsu, who runs the Office of the Comptroller of the Currency (OCC) and supervises approximately 1,000 national banks, some U.S. banks may have become “so big and complex that control failures, risk management breakdowns and negative surprises occur too frequently—not because of weak management, but because of the sheer size and complexity of the organization. In short, effective management is not infinitely scalable.”

And while investors have taken a dim view of smaller banks this year, selling off shares and withdrawing deposits often in a panic, they don’t seem to be enamored with universal Wall Street banks either.

A December 2022 study by McKinsey, a management consultancy, stated that America’s banking industry was “the lowest-valued sector in the world in 2021.” Investor sentiment grew even worse in 2023; banks started the year trading at an average 40 percent premium to their book value, but by April were trading at valuations equal to their book value.

This means that investors see banks as worth no more than their theoretical liquidation value. The average price-to-book-value for S&P 500 companies is currently 4.05.

The McKinsey report noted that banks’ profit margins had fallen by more than 25 percent over the past 15 years and were expected to fall another 20 percent over the next decade. It also predicted that banks’ return on equity, which has fallen from 15 percent in 2007 to 9.5 percent in 2021, would continue to decline in the coming years.

“Banking stocks trade at an accelerating discount to other industries—from a 15 percent discount in 2000 to a 70 percent discount in 2022,” the report stated. “This means that global investors are voting with trillions of dollars against the future profitability and sustainability of the existing model of universal banks.”

The consultancy deemed the banking industry “a $20 trillion breakup opportunity,” which, though unmentioned in the report, would also be a lucrative opportunity for consulting fees.

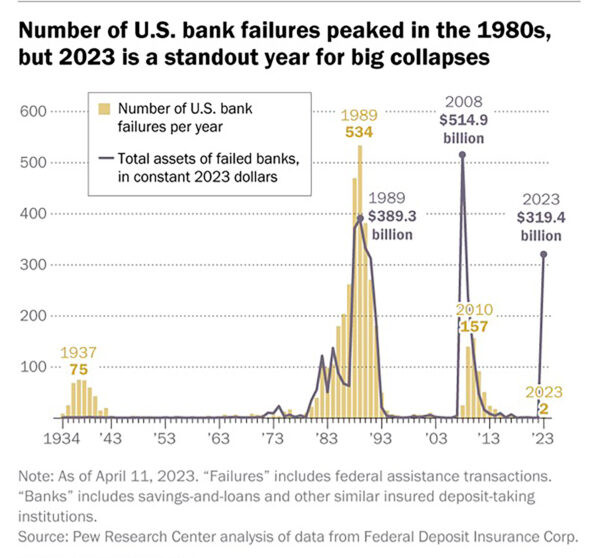

The number of banks operating in the United States has declined steadily, with several episodes of rapid decline. Coming out of the Great Depression in the 1930s, the number of commercial banks in the United States held steady for decades at between 13,000 and 14,000. Then, starting in the 1980s, that number began to fall, until eventually reaching today’s level of about 4,800 banks.

The savings and loan crisis of the 1980s featured banks with long-term fixed rate asset portfolios, typically mortgages and property loans, that were squeezed by rising interest rates. As a result of this crisis, 6,000 banks went bust. This was followed by the “Great Financial Crisis” of 2008, when massive defaults in mortgages threatened the stability of the entire financial system.

The savings and loan crisis was similar to today’s regional bank crisis, which so far has been mostly limited to regional banks with large amounts of uninsured deposits that were invested in longer-term fixed rate assets. These banks, including Silicon Valley Bank (SVB), Signature Bank and, most recently, First Republic Bank, were caught by rising interest rates.

America’s financial markets are unique, the result of historical efforts to diversify risk, preserve community banking and protect depositors. The National Bank Act of 1863, and later the McFadden Act of 1927, prohibited banks from being owned and operated across state lines. In an effort to protect depositors, the Glass-Steagall Act of 1933 established the Federal Deposit Insurance Corporation (FDIC) and separated banks that dealt in stocks and bonds from banks that took in deposits.

The result was a wide array of banks, from fast-dealing Wall Street investment banks to mammoth commercial banks to small local and regional banks. But, fearing that banks with concentrated exposure to a single state or region created excessive risk for the financial system, Congress passed the 1994 Interstate Act, which allowed banks to branch across state lines.

In 1999, the Financial Services Modernization Act repealed the provisions in Glass-Steagall that separated deposit-taking and investment banking. This led to a wave of mergers and acquisitions between commercial and investment banks, resulting in the absorption of storied firms like Salomon Brothers, First Boston, Bear Stearns and Merrill Lynch, by large “universal banks.” And the universal banks themselves merged with, for example, JPMorgan Chase and Bank One merging to become JPMorgan Chase, and Wachovia bank being absorbed by Wells Fargo.

For Americans, this trend of mergers and tighter collaboration with government, dubbed the “Great Consolidation,” may ultimately lead to a dearth of banking services for individuals, small businesses and smaller communities, as well as fewer opportunities for banks to innovate and serve customers profitably. It has also ushered in an era in which Wall Street takes on a larger role in politics, even as the federal government takes on a stronger role in directing Wall Street.

Venturing into politics in his 2022 letter to shareholders, JPMorgan Chase CEO Jamie Dimon, stated that “we need to find a way to more rapidly reorganize our government for the new world,” and called for the United States to embark on an industrial policy, which means “the federal government, through incentives and policies, drives American industry,” to foster industries such as batteries, rare earths, semiconductors, or electric vehicles.

“We may even need to evoke eminent domain,” he wrote, referring to government seizure of Americans’ land, in order to build out a “green” energy infrastructure. But “rest assured, your CEO is a red-blooded, patriotic, free-enterprise, and free-market capitalist (properly regulated, of course),” Dimon stated.

In 2022, the “Big Four” banks—JPMorgan Chase, Bank of America, Citibank and Wells Fargo—collectively spent billions on progressive political causes. Bank of America CEO Brian Moynihan, for example, stated in his 2022 shareholder report that the bank “intends to “deploy $1.5 trillion in sustainable finance by 2030, $1 trillion of which is aligned to the environmental transition and $500 billion to inclusive social development.”

This includes Bank of America’s $2 billion Equality Progress Sustainability Bond, which will “help advance racial and gender equality, economic opportunity, and environmental sustainability.” JPMorgan Chase and Bank of America also reportedly provide financing to certain favored races on preferential terms.

Currently, 95 percent of Americans have bank accounts. However, the trend among banks is to close branches, particularly in rural, remote, and low-income communities.

According to a report by S&P Global Market Intelligence, nearly 3,000 bank branches were closed across the United States in 2021. Wells Fargo, the most aggressive in shutting down branches, closed 267 of them. Overall, the five states with the most branch closures were California, with 269 branch closures; Michigan, with 247; New York, with 221; Florida, with 192; and Illinois, with 153.

“America’s capital markets remain very competitive by global standards,” Gregg said. “But as they become ever more tightly regulated, the less competitive they will become, because large banks can absorb the cost of ever-more regulation in ways that medium and small-sized banks cannot.”

In addition, he said, “it is possible that a smaller number of banks may result in the banking industry becoming less interested in backing new entrepreneurs and startups, as well as giving less attention to existing small and medium-sized businesses, because large banks will tend to gravitate toward focusing on big clients.”

Part of the trend of branch closures is the result of fewer people visiting bank branches, due to the rise of the fin-tech industry. Banks are now facing competition from big tech with the increasing acceptance of new technologies like payment apps, including PayPal, Venmo, Apple Pay and Google Pay. And the rise of online banking also allowed customers at banks like SVB to pull their deposits out of the bank immediately without having to visit a branch, following rumors that the bank was in trouble that spread over social media.

At the same time, some areas of banking have been taken over by speciality companies, creating what Bowman called the “shadow banking” industry that largely operates outside the banking regulatory framework. This includes not only the fin-tech industry, but also companies like mortgage lenders.

“Mortgage origination and servicing—both long-standing, traditional banking activities—shifted onto nonbank entities following the 2008 financial crisis,” Bowman said. In 2020, 68 percent of new mortgages were issued by mortgage companies and other nonbank institutions. Nonbank lenders are also stepping into other areas, like corporate loans, farm loans, commercial real estate, and consumer lending.

And while the “shadow banking” system may be encroaching on banks’ profits, they are not necessarily relieving banks of risk.

“The growth of lending in the shadow banking system can have significant consequences for the availability of credit over economic cycles, with losses eventually being transferred to regulated depository institutions, as appears to have occurred after the 2008 financial crisis,” Bowman said. “While [these] activities may be pushed out of the regulated banking system, losses may be transmitted back into the banking system through related activities like the extension of credit by banks to those same nonbank lenders.”

Discount Applied Successfully!

Your savings have been added to the cart.