As of 7:37 a.m. EDT, Wednesday, April 22, 2026, front‑month WTI is trading at $90.58 and Brent at $99.56…a near‑$9 spread that screams “seaborne stress plus U.S. advantage.” The U.S. Dollar Index is hovering in a firm, high‑90s zone, consistent with a risk‑aware, geopolitically tense backdrop, even as markets start to absorb Middle East tensions rather than panic over every headline.

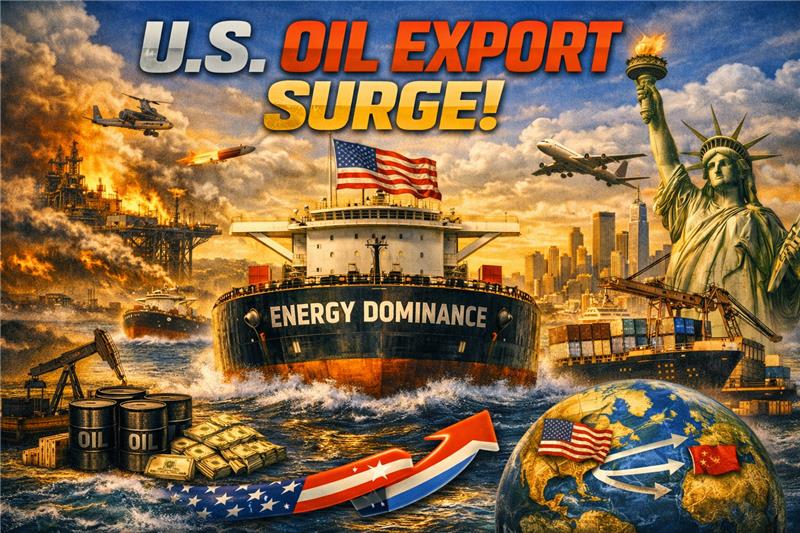

Oil Near $100: The Day the World Quietly Crowned America the New Energy Superpower

By George Magazine

The backdrop: war risk that markets are learning to live with

- Iran war & Hormuz: The conflict with Iran keeps the Strait of Hormuz partially impaired…flows are reduced, insurance and freight remain expensive, and any tanker incident can still move prices.

- From shock to regime: Early‑war spikes have cooled into a new “war regime”: traders now assume persistent disruption, not immediate collapse, and are pricing in a long conflict tail rather than a one‑off shock.

- Result: Brent holds a high‑90s handle, reflecting seaborne risk, while WTI trades lower but elevated, reflecting U.S. security of supply plus export demand.

U.S. exports: the swing barrel of the world

- Record‑style flows: U.S. Gulf Coast terminals (Corpus Christi, Houston, LOOP) are pushing multi‑million‑barrel‑per‑day exports, effectively acting as the world’s emergency loading dock.

- Europe: Having already pivoted away from Russian crude, European refiners are now structurally more dependent on U.S. light sweet barrels, which avoid the Hormuz chokepoint and come with lower geopolitical risk.

- China & Asia: China buys more tactically…leaning on discounted Russian and regional grades, but pulling in U.S. cargoes when the Brent–WTI spread, freight, and politics line up.

Net effect: the center of export growth has shifted decisively toward the United States, even though the Middle East still matters on volume.

Shift away from the Middle East

- Risk premium: Middle Eastern barrels carry a war and logistics premium…higher insurance, higher perceived risk, and occasional physical disruption.

- Contract behavior: Buyers are locking in term deals with U.S. suppliers and diversifying away from Gulf dependence, especially for grades that can be easily substituted by U.S. crude.

- Structural change: This isn’t just a short‑term scramble; it’s nudging refiners and traders to re‑anchor supply chains around the U.S. Gulf and Atlantic Basin.

Boost to the U.S. economy

- Cash flow & capex: Elevated prices plus strong export volumes mean robust cash flow for U.S. producers, midstream firms, and shippers…supporting new investment in pipelines, terminals, and fleets.

- Jobs & tax base: Gulf Coast regions benefit from higher employment, service demand, and tax revenues, reinforcing local and national growth.

- Trade balance: Crude and refined‑product exports help improve the U.S. trade balance, partially offsetting deficits elsewhere.

The drag: U.S. consumers still face relatively high fuel prices, so some of the macro gain is offset by pressure on households and non‑energy businesses.

Dollar strength and other oil markets

- Firm dollar: A strong Dollar Index in the high‑90s usually leans against commodities by making them pricier in local currencies. Here, physical tightness and war risk are strong enough that crude holds a $90+ handle anyway.

- Global squeeze: For Europe and emerging markets, firm dollar + high oil is a double squeeze…energy costs rise in local terms while financial conditions tighten.

- Spreads & curves:

- Brent–WTI spread (~$9) reflects seaborne tightness and direct Middle East exposure.

- Backwardation in time spreads signals that prompt barrels are more valuable than future ones, classic tight‑market behavior aligned with strong U.S. exports and constrained Gulf supply.

What to expect in today’s trading

With WTI around $90–91 and Brent near $100:

- Base case: A headline‑sensitive but relatively contained session…the market has seen this movie for weeks and is less jumpy.

- Bullish triggers: Any new tanker incident, infrastructure strike, or breakdown in talks could push Brent decisively above $100 and widen the spread further, reinforcing demand for U.S. barrels.

- Bearish/relief triggers: Credible signs of de‑escalation or improved maritime security could bleed off some war premium, nudging prices lower but likely keeping WTI in the high‑80s/low‑90s zone.

- Equities: U.S. energy producers, midstream, and shipping names stay relatively supported; fuel‑intensive sectors and rate‑sensitive names remain under pressure from the combo of high energy and a firm dollar.

*****

Get Ageless Tech A.I.-Using AI to Your Advantage: https://georgemagazine.com/agelesstech/

Get George’s America’s 250th: https://georgemagazine.com/product/america-250-celebrating-legacy/

Get The George Dispatch: https://georgemagazine.com/thedispatch/

Get George Magazine. Print or Digital: https://georgemagazine.com/subscribe-george-magazine/

Get George Junior. Print or Digital: https://georgemagazine.com/subscribe-george-junior-magazine/

Get George’s Crypto E-Playbook: https://georgemagazine.com/product/the-crypto-playbook-by-george-magazine/

Continue reading your articles with a George Magazine Subscription.

Subscribe to Access Your Free Guide & Images

Subscribe to George Magazine and unlock exclusive bonuses. Your subscription now includes a free crypto essentials guide and three premium downloadable images. These images are perfect for personal use as desktop or mobile backgrounds, with thumbnail previews shown below.

Already a subscriber? Please log in and try again.

LoginOne thought on "Oil Near $100: The Day the World Quietly Crowned America the New Energy Superpower"

Leave a Reply

-

CO(v)F(e)FEE Mug, 20oz

$15.42 Select options This product has multiple variants. The options may be chosen on the product page -

New Hollywood – GEORGE Issue 4, The White Cover

Price range: $15.57 through $22.08 Select options This product has multiple variants. The options may be chosen on the product page -

Editor’s Journal

$13.70 Select options This product has multiple variants. The options may be chosen on the product page -

Who runs the world?

Price range: $15.57 through $22.08 Select options This product has multiple variants. The options may be chosen on the product page

Discount Applied Successfully!

Your savings have been added to the cart.

This is a remarkable analysis of the oil industry. Good by OPEC – we don’t need your black gold anymore- Hello to the New America! Do you want to keep it going! Then vote everyone!