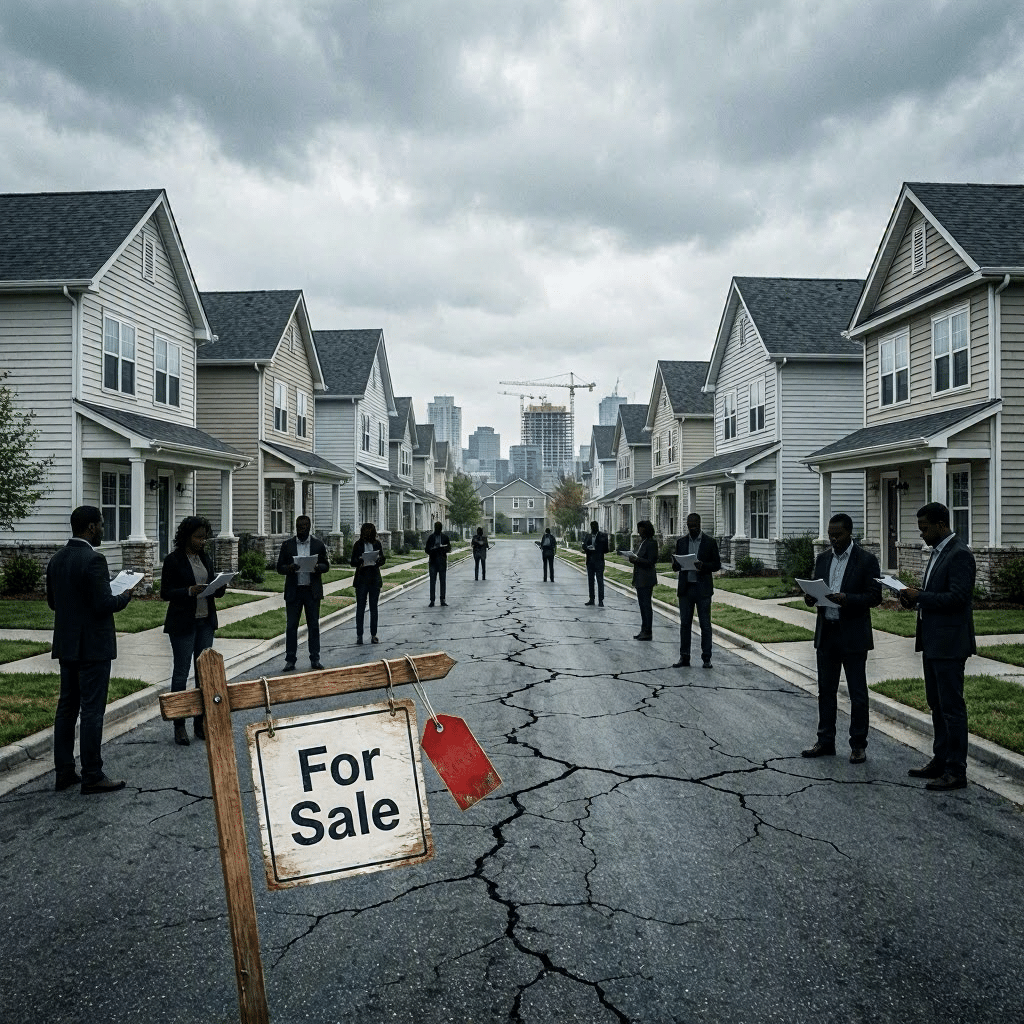

1. The Core Causes

• Severe Housing Shortage (the #1 driver)

The U.S. is short an estimated 3.5–5.5 million homes, depending on the source. Builders under‑built for more than a decade after the 2008 crash, and zoning restrictions in major metros choke supply. This shortage alone keeps prices elevated even when demand cools.

• Mortgage Rate Shock

Rates jumped from 2.7% to 7–8% in two years…the fastest increase in modern history. This didn’t crash prices because it froze supply:

- 92% of homeowners have mortgages under 5%.

- They refuse to sell and give up their low rate.

This “lock‑in effect” created the lowest inventory in 40 years.

• Institutional Buyers & Cash Dominance

Wall Street firms, private equity, and cash investors now represent 25–33% of purchases in some markets. They don’t care about mortgage rates, which keeps competition high for the limited homes available.

• Demographic Pressure

Millennials…the largest generation…are in peak home‑buying age. Demand is structurally strong even when affordability is weak.

• Construction Costs & Labor Shortages

Materials, land, and labor costs remain elevated. Builders can’t profitably produce “starter homes,” so they focus on higher‑margin properties, worsening the affordability crisis.

2. So Is It a Bubble?

Not in the traditional sense. Prices are high because supply is broken, not because of reckless lending or speculative flipping. Unlike 2008:

- Credit standards are tight.

- Subprime lending is minimal.

- Homeowners have record equity.

- Delinquencies remain historically low.

This is a housing affordability crisis, not a speculative bubble.

3. What Could Cause a Correction?

A meaningful price decline would require one of the following:

- A surge in unemployment

- A wave of forced selling

- A major increase in housing supply

- A rapid drop in investor demand

- A credit crunch

None of these are happening at scale today.

4. How This Ultimately Resolves

• Gradual Price Softening, Not a Crash

Most economists expect sideways-to-slightly-down prices over several years, not a collapse.

• Mortgage Rates Slowly Normalize

If rates drift back toward 5%, demand will rise…but so will supply as locked‑in owners finally move.

• Policy & Zoning Reform

Some states are already legalizing duplexes, ADUs, and higher-density zoning. This is slow but necessary.

• Build-to-Rent Expansion

Institutional builders will continue producing rental communities, increasing supply indirectly.

• Long-Term: Supply Catch-Up

The market stabilizes only when construction finally meets demographic demand…a process that may take 5–10 years.

*****

Get “Co V Fe Fe” Shirt here: https://georgemagazine.com/product/cov-fe-fe-george-magazine/

Get the Aetherian Realm’s Final Judgments Map: https://georgemagazine.com/product/aetherian-realms-final-judgments-map/

Get Ageless Tech. Using AI to Your Advantage: https://georgemagazine.com/agelesstech/

Get George’s America’s 250th: https://georgemagazine.com/product/america-250-celebrating-legacy/

Get America’s 250th George Magazine T-Shirt: https://georgemagazine.com/product/americas-250th-george-magazine-t-shirt/

Get The George Dispatch: https://georgemagazine.com/thedispatch/

Get George Magazine. Print or Digital: https://georgemagazine.com/subscribe-george-magazine/

Get George Junior. Print or Digital: https://georgemagazine.com/subscribe-george-junior-magazine/

Get George’s Crypto E-Playbook: https://georgemagazine.com/product/the-crypto-playbook-by-george-magazine/

Visit Project Looking Glass: https://projectlookingglass.org/

![[GOOD PRESS] ON[GOOD PRESS] ON](https://georgemagazine.com/wp-content/uploads/2024/08/16389056566437433941_2048-300x300.jpeg)

![Enjoy the [Road] Show Travel Mug with Handle, 14ozEnjoy the [Road] Show Travel Mug with Handle, 14oz](https://georgemagazine.com/wp-content/uploads/2024/08/479070202831754764_2048-300x300.jpeg)